The consolidated results on open position enable you to compare the exposure (Commercial Transactions in forecast mode) with the actual financial hedging (Spot, Forward Exchanges and Swaps). This comparison enables you to calculate the global result, to identify the existence of over and underhedgings, to determine the efficiency of the risk hedging strategy set up by the treasurer and to value the open position.

The valuation of the exposures and hedging is made on the basis of the market rates, according to the mark-to-market method, by comparing the transaction rate with the revaluation rate, in order to calculate the actual and potential results. You can recognize the imported amounts from the exported amounts for the transactions expressed in the company currency (for the analysis of a single company result) or in the consolidation currency (for multiple company selections).

Info

The results on Cash Transactions (currency borrowings and loans) are not integrated into the consolidated results as they do not use the same approach of performance (acquired result) and hedging analyses.

To customize results, the FX module proposes to revalue commercial transactions on the basis of the three following exchange rates:

- the budget rate, determined during the analysis,

- the opportunity rate (forward rate at transaction date),

- the settlement rate (spot rate at delivery date).

The average rate for Commercial Transactions is then compared with the average rate of the actual FX transactions, which enables the calculation of an actual and potential result with the distinction between import and export.

The open position equals the financial position minus the commercial position. It is revalued (in forecasted result) according to one of the three following exchange rates chosen by the treasurer:

- a spot rate at a determined date,

- the forward rate calculated according to the average maturity, with a monthly step, of the open position,

- a simulated rate, determined by the treasurer.

Info

FX Transactions are valued at the initial rate assigned at the time of their entries, and expressed in the company currency.

For an exposure of USD 1,000, 800 are hedged for the maturity. The open position amounts to USD 200 with 100 within 3 months and 100 within 9 months. The calculated average maturity equals 6 months. A theoretical forward rate is also proposed.

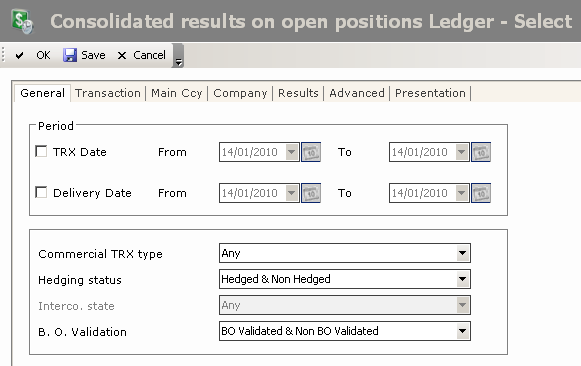

- From the Modules Tasks pane, select the Consolidated Results on Open Positions option in the Report folder of the FX module.

- If no filter has been set up for this report, the creation page for filters is displayed. You first need to create a filter.

This filter enables you to select the commercial transactions and the FX transactions to display according to your criteria.

View the topic below for more information on the creation of selection filters for Commercial and FX Transactions.

- If a filter has already been set up, the modification page for filters appears with the default filter settings.

If you need to modify the filter settings, see below the topic regarding filters creation.

- Click OK to view the report with the filter settings.

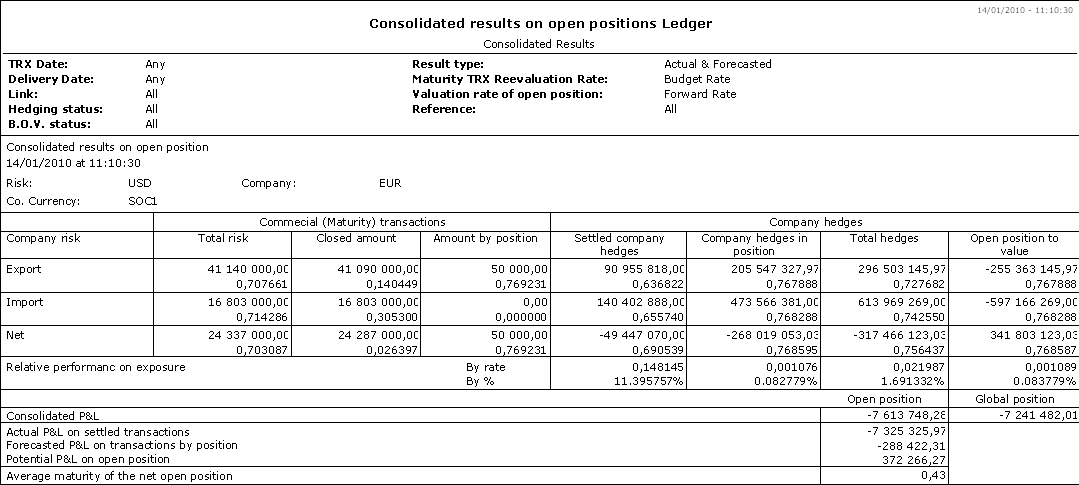

The header displays the report name, as well as the filtering criteria defined in the report filter (see the topic below for more information on this type of filter).

The body of the report presents a table with the details of the consolidated results on open position.

Commercial Transactions and the actual FX transactions (spot, forward exchanges and swaps) are sorted by company, by currency and then, according to your filtering criteria, by export and/or import risk.

The total actual result on Commercial Transactions is calculated, for the import and/or export, with the details of the amount in position and of the remaining amount. You can directly compare the rates of your risks with the set up actual hedging, in order to obtain the actual result, the forecasted result and the potential result which all correspond to the hedging that can be set up for the open position.

This is an analysis of the global performance.

The total absolute performance of the actual hedging is also calculated. There is a distinction between the amount of the settled hedging and the amount of the hedging in position for the import and/or export sections.

The open position is the difference between the commercial position and the financial position. The treasurer chooses to revalue it at the spot or forward rate adjusted on the average maturity of the position.

A negative open position corresponds to a net over-hedging. A positive open position corresponds to a net under-hedging.

The relative performance in rate and percentage is calculated in rate and percentage. It enables the comparison of the hedging result with the company's objectives.

For hedging, there are three different levels of results:

- the actual result (on settled transactions),

- the forecasted result on the transactions in position (actual hedging),

- the potential result on open position (risks to be hedged).

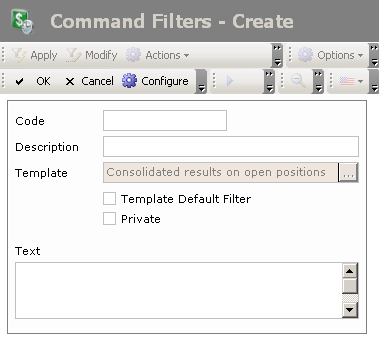

- To access the creation page for filters from the report page of the Consolidated Results on Open Position, click the Actions dropdown menu in the filters toolbar, and select the Add option.

The creation page for filters is displayed.

This page enables the definition of unique identification information for the filter.

- Enter a code and a description for the filter in the Code and Description fields.

- If you want this filter to be applied by default when you access the report page, enable the Template Default Filter option.

- If you want this filter to be only accessible by yourself, select the Private option.

- You may add a comment in the Text area.

- Click the Configure button to set up the filter settings.

The configuration page for filter settings is displayed.

If you want to copy the settings of an existing filter, click the Copy From button in the action bar. Click here for more information.

Info

If you do not specify any filtering criterion for the transactions in the different tabs of this page, the report will include all the existing FX transactions.

The General tab enables you to specify filtering criteria on the transaction and delivery dates of the transactions to include in the report, as well as filtering criteria on Commercial Transactions.

- To define a filtering process on the transaction date:

- Enable the option TRX Date.

The fields next to the option are enabled.

- In these fields, specify the start and end date of the period, between which must fall the transaction date of the transactions to include in the report, by going through the following process:

- In the entry field, select the value to modify and enter a date with the format dd.mm.yyyy.

- or -

- Click the

button to display the calendar.

button to display the calendar.

A contextual window displays the calendar.

Use the arrows  and

and  to select the month, year and day.

to select the month, year and day.

- or -

To set the start date to today's date, click the button Today.

- To specify a filtering process on the delivery date, enable the Delivery Date option, then go through the same process as above, to define the start and end dates of the period, between which must fall the delivery date for the transactions to include in the report.

- In the Commercial TRX Type dropdown list, select the direction of the commercial transactions to integrate into the result calculation:

- All to cancel any filter at the level of the direction of Commercial Transactions,

- Export Receipts to include only the commercial transactions with the receipts (export) type and the FX transactions with the sell type,

- Import Disbursements to include only the commercial transactions with the disbursements (import) type and the FX transactions with the sell buy.

- In the Hedging Status dropdown list, select the following option:

- Hedged & Non-Hedged to disable the filtering process on the commercial transactions hedging.

- Hedged to include the hedged commercial transactions only,

- Non Hedged to include the non-hedged commercial transactions only,

- In the BO Validation dropdown list, select one filtering criterion on the back-office validation of the transactions:

- BO Validated and Non BO Validated to disable any filtering process on the back-office validation,

- Non B.O. Validated to select the non-BO-validated transactions only,

- B.O. Validated to select the BO-validated transactions only.

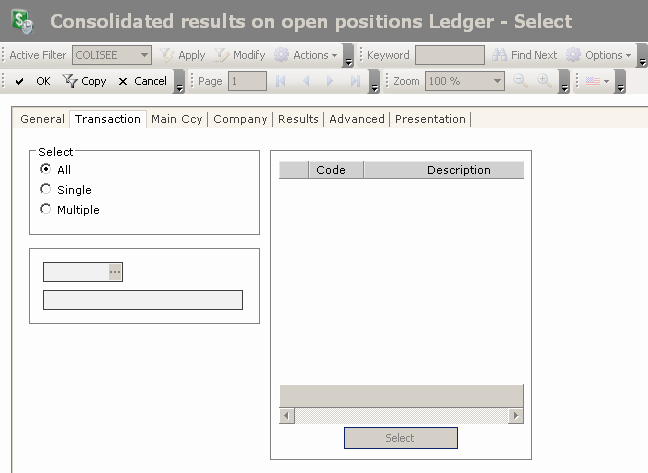

- Click the Transactions tab.

This tab enables you to specify filtering criteria on the type of the FX transactions to include in the report.

- In the Select area, enable the following option:

- All not to apply any filtering on the transaction types,

- Single to include only the FX transactions with the type selected in the area below,

- Multiple to include the FX transactions with one of the types selected in the area on the right.

- In the Select area , if you selected the following option:

- Single, select a transaction type by clicking the button

in the area below, then, in the contextual window, double-click your transaction type;

in the area below, then, in the contextual window, double-click your transaction type; - Multiple, select several transaction types as described below.

- On the right of the Select area, click the Select button.

- In the contextual window, enable the options in front of the transaction types to select, and click the

button at the top of the window.

button at the top of the window.

The codes and descriptions for the selected transaction types are displayed in the table of the area.

The Main Ccy and Company tabs look like the Transaction tab. Go through the same process as for the filtering on the main currencies and the associated companies in the previous tab.

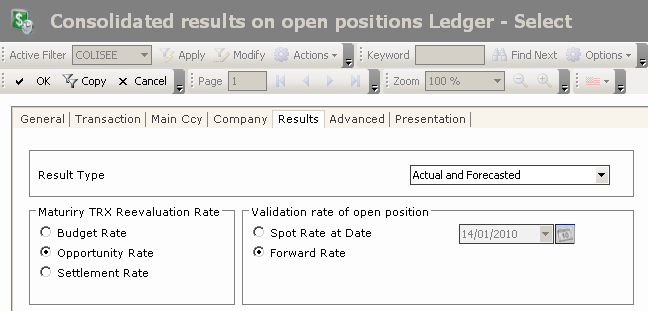

- Click on the Results tab.

This tab enables you to configure the settings for the result validation: result type (actual and/or forecasted) and rate to keep for Commercial Transactions and the open position.

Info

FX Transactions are validated at the transaction rate.

- In the Result Type dropdown list, select one of the options below, which enables you to determine the type of the validation rate.

- Actual: The actual result is calculated on the basis of the commercial and FX transactions revaluation, according to the contractual rate in effect at the payment date.

- Forecasted: The forecasted result is calculated on the basis of the potential revaluation of transactions, according to the forward market rate. This valuation corresponds to the valuation at the historical cost, based on the mark-to-market principle.

- Actual and Forecasted: The forecasted result and the actual result are automatically calculated.

- In the Maturity TRX Revaluation Rate area, enable the option corresponding to the revaluation basis for Commercial Transactions.

- Budget Rate: This is the monthly budget rate of the commercial transactions currencies, which may have been modified. This option is selected by default.

- Opportunity Rate: This is the forward market rate at which the transaction would be actual if it was hedged at the transaction date.

- Settlement Rate: This is the spot market rate at the settlement date, it is determined on the delivery day of the currencies — the rate at which the position without hedging would have been settled.

Info

You cannot select the spot rate at the settlement date if you selected the Forecast option in the Result Type dropdown list.

- In the Validation Rate of the Open Position area, enable one of the following options which enables the determination of the rate type used for the revaluation of the open position.

- Spot Rate at Date: The spot rate on the specified date is used.

If you enable this option, select a date in the adjacent field by entering a date in the dd/mm/yyyy format or by using the calendar which can be accessed from the button, as explained previously.

- Forward Rate: The forward rate is used. Its calculation is based on the average maturity of the open position. This average maturity corresponds to the average duration of the monthly net position weighted by the volumes. The forward rate enables the determination of the average rate resulting from actual market data, in order to hedge the non-hedged part (open position) or to rebuy the over-hedged part (over-hedged position).

With an exposure by USD 100,000, USD 80,000 are hedged forward. The open position amounts to USD 20,000. For these USD 20,000 to be hedged, FX identifies the average maturity (USD 10,000 within 3 months, USD 10,000 within 9 months) which corresponds to 6 months, and proposes a theoretical forward rate which enables the calculation of the potential result.

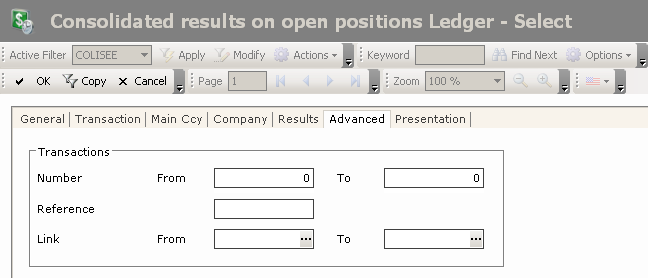

- Click on the Advanced tab.

This tab enables you to specify filtering criteria on the order numbers, the external reference and the link numbers of the transactions to include in the report.

- In the Number field of the Transactions area, enter a range of order numbers for Commercial and FX Transactions.

Important

They are not the complete numbers of transactions, but the numbers of the creation order, they can be found on the right of transactions numbers. The transaction number consists of the company code, the transaction type code and the transaction order number.

- In the Link field, enter a range of link numbers for FX and Commercial Transactions, or select a range using the button as explained previously.

- In the Reference field, enter the external reference number for FX and Commercial Transactions.

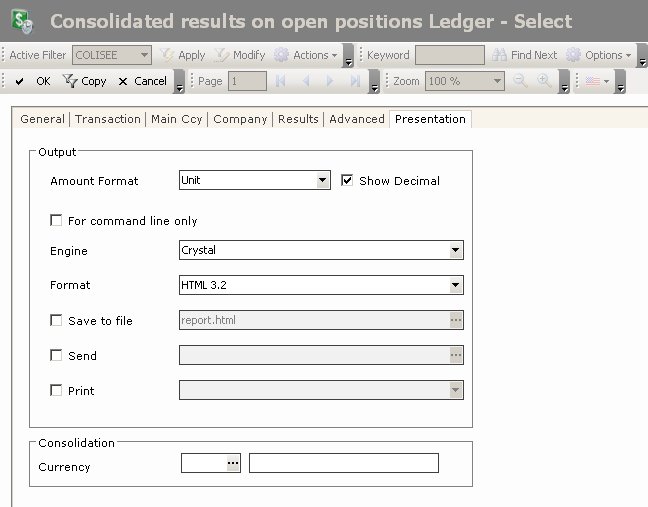

- Click on the Presentation tab.

This tab enables you to specify the output formats for the report.

- Complete the fields described in the table below.

| Field | Description |

|---|---|

| Amount Format | Select the display unit for amounts in the dropdown list. |

| Show Decimal | Select this option if you want to see the digits after comma in the amounts. |

| For command line only | Select this checkbox to launch a report through the command line only. |

| Engine | In this dropdown list, select the software to use for report creation. |

| Format | In this dropdown list, select the format of the output file. |

| Save to file | Click the button, then, in the contextual window, select the name and location of the output file. |

| Send | Click the button, then, in the contextual window, select the recipients of the e-mail including the report. The address book is the default one associated with your messaging account. |

| Select a printer for the printing of the report. |

- In the Currency field, select the currency for the amounts consolidation in the report using the button .

- Click OK to confirm the filter creation and view the report with the new filter settings.